Juggling multiple balances can feel like spinning plates that never stop wobbling. One bill is due today, another next week, and the interest keeps stacking up in the background. Debt consolidation loans exist to simplify that chaos by turning several balances into one structured plan. In the first few months alone, many borrowers notice clearer budgeting and fewer surprises.

According to the Federal Reserve, U.S. households carry trillions in revolving debt, with credit cards holding some of the highest average interest rates in consumer finance. That reality explains why so many people search for ways to regain control without extreme measures. Instead of guessing your next move, a smarter structure can help.

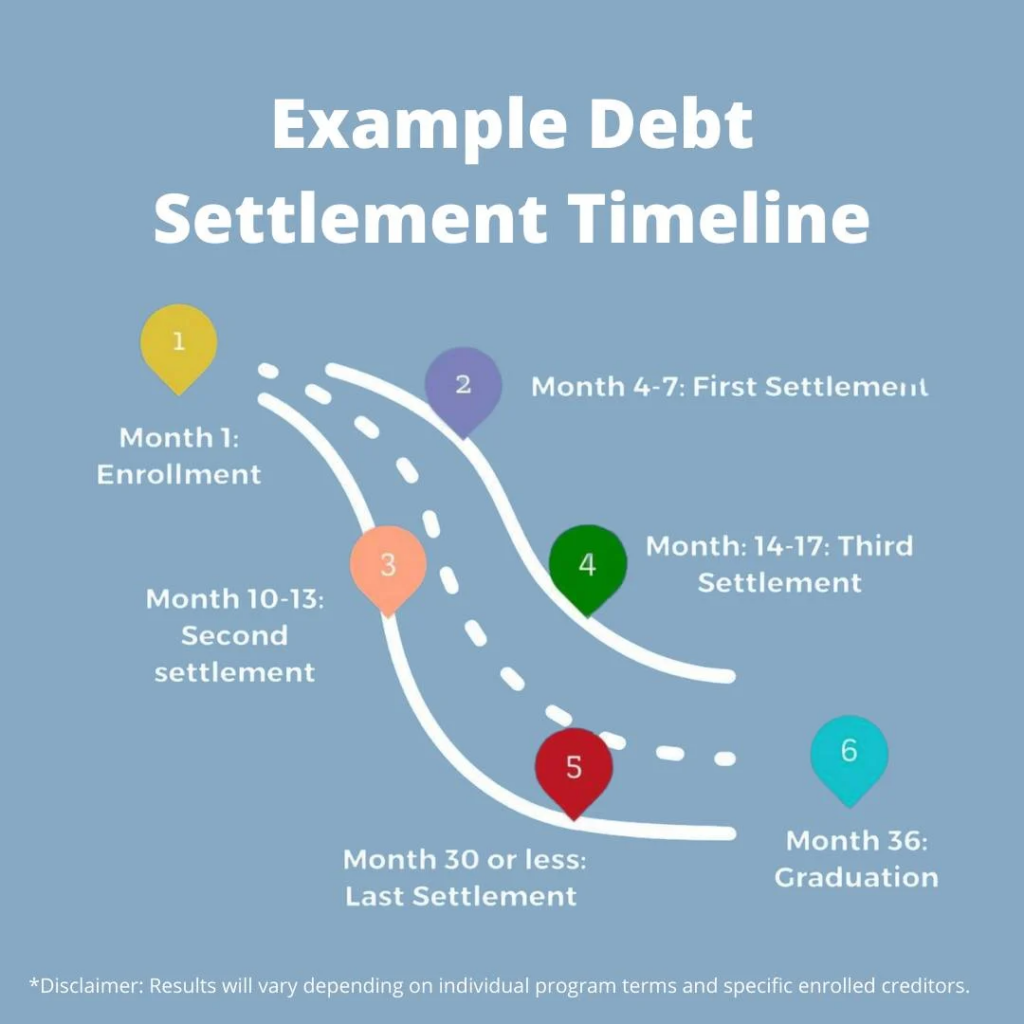

Here’s everything you need to know.

Debt Consolidation Loans and How They Actually Work

Debt consolidation loans combine multiple unsecured debts into one installment loan with a fixed payment and clear payoff timeline. Credit cards, medical bills, and other personal debts get paid off upfront, then replaced by a single lender relationship.

This approach is commonly used as one of several debt relief options for people who still have steady income and want predictability. The Consumer Financial Protection Bureau explains that installment loans often carry lower rates than revolving credit, especially when credit cards charge APRs above 20%.

Typical features include:

| Feature | What to Expect |

| Loan amounts | $2,500–$45,000 |

| Terms | 24–60 months |

| Rates | Fixed, based on credit profile |

| Payment | One monthly due date |

This structure supports planning and reduces the mental load tied to multiple accounts.

How Personal Loan Consolidation Changes Your Monthly Budget

Using personal loan consolidation shifts debt from variable payments to a single fixed obligation. That change alone often improves cash flow clarity.

A real-world example reviewed in client case files shows a borrower carrying $18,000 across four cards at an average 23% APR. After consolidation into a 36-month loan near 12%, the monthly total dropped by over $250. That reduction made room for savings while shortening the payoff timeline.

This method is frequently used for credit card debt help because it removes rotating balances and replaces them with a schedule that actually ends.

Americor Funding and Its Debt Consolidation Loan Solutions

Americor Funding offers access to debt consolidation loans through a structured, consultation-first process. Headquartered in Irvine, California, the company operates as a debt relief organization that evaluates each financial situation before recommending a solution.

Americor Funding works with lending partners to provide consolidation loans typically ranging from $2,500 to $45,000. These loans are designed to pay off credit cards and other unsecured debts, then replace them with one fixed monthly payment over a set term.

What sets Americor Funding apart is its dual-path approach. If consolidation fits your income, credit profile, and goals, loan options are reviewed in detail. If it does not, alternative strategies are discussed instead of forcing approval. This model helps borrowers avoid taking on loans that do not truly improve their financial position.

Why Lower Monthly Debt Payments Matter More Than You Think

Smaller, predictable payments support consistency. Missed or late payments often happen due to confusion, not intent. Consolidation reduces that risk by offering lower monthly debt payments tied to one date.

From a credit perspective, paying off cards also improves utilization ratios. FICO scoring models treat installment loans differently than revolving credit, so this shift may support gradual score recovery when payments stay on time.

High Interest Debt Solutions That Focus on Stability

Credit cards remain one of the most expensive borrowing tools available. Federal Reserve reports consistently show card APRs far higher than most personal loans. That difference explains why consolidation remains one of the most effective high interest debt solutions available.

Fixed rates protect balances from future increases and make repayment costs easier to forecast, especially during periods of economic uncertainty.

Credit Card Refinancing Compared With Balance Transfers

Credit card refinancing through a consolidation loan works differently than promotional balance transfers.

- Balance transfers often expire within a year

- Transfer fees usually range from 3%–5%

- Rates may rise sharply after promotions end

Installment loans keep the same terms from start to finish, making them better suited for balances that need time to resolve.

Debt Payoff Strategies That Support Long-Term Results

Consolidation works best when paired with smart habits. Financial counselors often recommend these debt payoff strategies:

- Limit access to cleared credit cards

- Build a starter emergency fund

- Track progress monthly

Data from the National Foundation for Credit Counseling shows consumers who monitor repayment milestones are more likely to complete their plans successfully.

Limitations and Common Concerns

Consolidation does have boundaries. Approval depends on credit profile, income stability, and debt-to-income ratios. Fees can also reduce upfront savings, so reviewing the full APR matters.

Another concern involves spending behavior. Consolidation reorganizes debt but does not erase it. Without adjustments, new balances may undo progress. Financial advisors consistently stress that behavior change supports long-term results.

A Clear Path Forward

Debt relief does not need to feel overwhelming or extreme. When structured carefully, consolidation can support clarity, reduce stress, and simplify repayment without sacrificing credit health. Reviewing offers, understanding terms, and choosing a plan that fits your income creates momentum that builds over time.

Finding options with a qualified provider and asking detailed questions helps ensure the solution fits your goals. Taking that step today can move your finances toward stability and confidence, one payment at a time.

Leave a Reply